- IRS forms

- Form 433-F

Form 433-F: Collection Information Statement

Download Form 433-FWhen facing tax-related debts or delinquencies, individuals or businesses may find themselves in the uncomfortable position of dealing with the IRS (Internal Revenue Service). As part of the collection process, the IRS may require taxpayers to complete Form 433-F, also known as the Collection Information Statement.

In this blog, we will delve into the details of Form 433-F, helping you understand its purpose, how to complete it accurately, and the implications it may have on your tax situation.

Purpose of Form 433-F

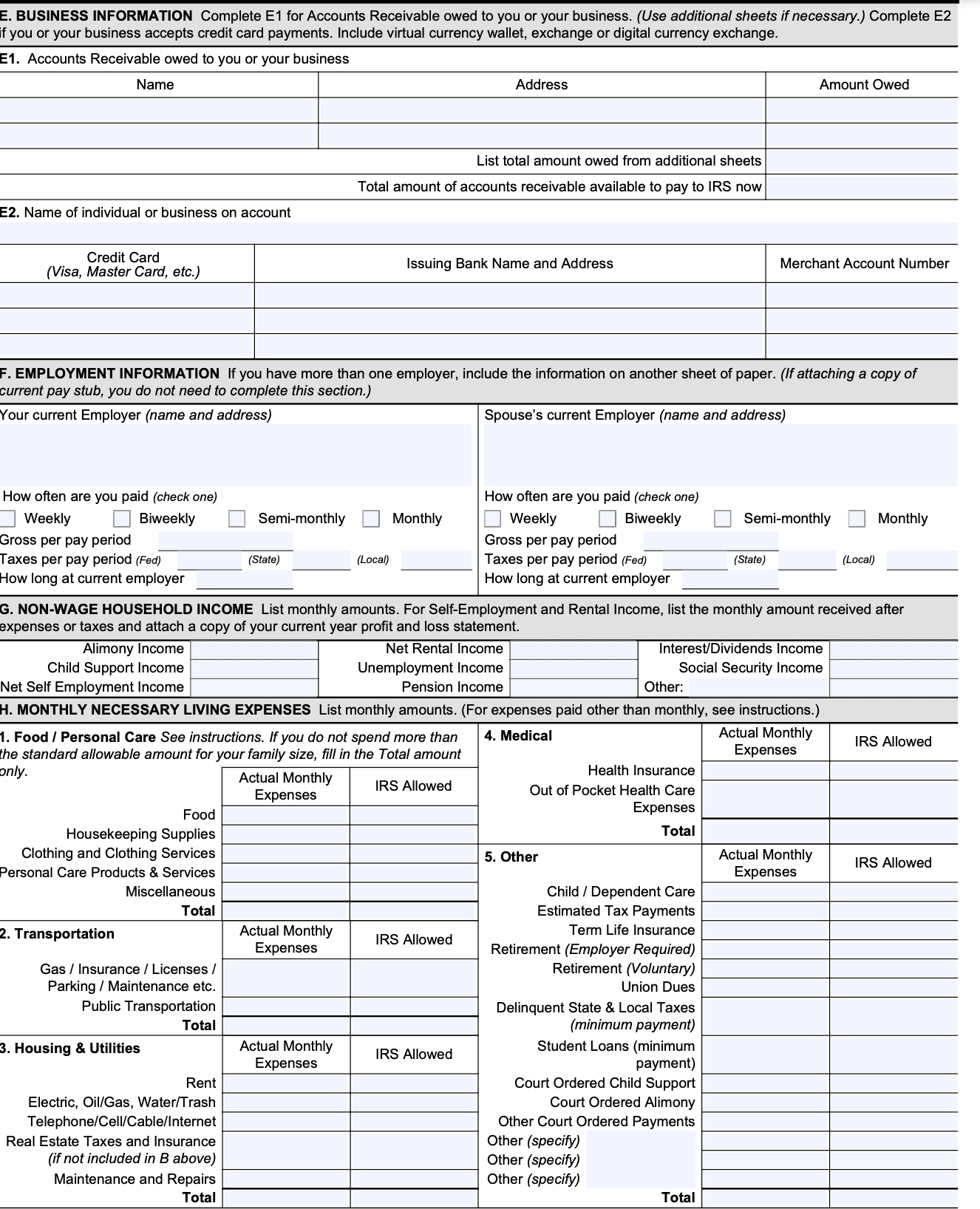

Form 433-F is a financial statement used by the Internal Revenue Service (IRS) in the United States. Its purpose is to collect information about an individual's or a business's financial situation in order to assess their ability to pay outstanding tax debts.

The form is typically used in cases where taxpayers owe back taxes and are unable to pay the full amount owed. It helps the IRS determine the taxpayer's ability to pay and establish an appropriate installment agreement or other payment arrangement.

By completing Form 433-F, taxpayers provide detailed information about their income, (link: https://fincent.com/blog/assets-liabilities-equity-key-differences-and-their-importance text: assets, expenses, and liabilities). This includes details about their employment, sources of income, bank accounts, real estate, vehicles, and other assets. Additionally, taxpayers must provide information about their monthly living expenses, such as housing, utilities, transportation, and medical costs.

Benefits of Form 433-F

While the primary purpose of Form 433-F is to assess the taxpayer's ability to pay and establish an appropriate payment plan, there are several benefits associated with its use:

Establishing a repayment plan: Form 433-F enables taxpayers to propose a suitable repayment plan to the IRS based on their financial circumstances. This allows individuals to pay off their tax debt gradually over time, making it more manageable and reducing the financial burden.

Avoiding collection actions: By submitting Form 433-F and entering into a payment plan, taxpayers can prevent or halt collection actions by the IRS. This includes measures such as wage garnishment, bank levies, or property seizures, providing relief from immediate enforcement actions.

Reduced penalties and interest: While interest and penalties may still apply, entering into a formal payment arrangement through Form 433-F can potentially reduce the overall amount owed. By demonstrating a good faith effort to resolve the tax debt, taxpayers may qualify for penalty abatement or other forms of relief.

Protection of assets: By cooperating with the IRS through the submission of Form 433-F, taxpayers can protect certain assets from being seized to satisfy the tax debt. The IRS may be more inclined to work with individuals who are proactive in resolving their tax issues rather than resorting to aggressive collection actions.

Resolving tax issues proactively: Completing Form 433-F and engaging in the payment plan process demonstrates a willingness to address (link: https://fincent.com/blog/what-is-income-tax-liability-and-how-do-you-calculate-it text: tax liabilities) responsibly. It allows individuals to take control of their tax situation and work towards full compliance, potentially improving their overall financial standing.

It's important to note that the specific benefits obtained from Form 433-F can vary depending on individual circumstances and the IRS's evaluation of the taxpayer's financial information.

Who Must File Form 433-F?

Form 433-F, Collection Information Statement, is typically filed by individuals or businesses who owe taxes to the Internal Revenue Service (IRS) and are unable to pay the full amount.

This form is used to provide the IRS with detailed financial information to determine an appropriate payment arrangement or alternative resolution options. It helps the IRS assess the taxpayer's financial situation and ability to pay their tax debt.

Generally, individuals and businesses who owe more than $50,000 in taxes and cannot pay the full amount immediately may be required to file Form 433-F. However, the exact threshold and requirements can vary based on individual circumstances and the discretion of the IRS.

It is important to note that Form 433-F is just one of several forms used for financial disclosure to the IRS in situations where taxpayers owe taxes but cannot pay the full amount.

How To Complete Form 433-F: A Step-by-Step Guide

Completing this Form 433-F accurately is important to establish a payment plan or negotiate an alternative solution with the IRS.

Here's a step-by-step guide to completing Form 433-F:

Step 1: Obtain the form.

You can download Form 433-F from the IRS website or request a copy by calling the IRS helpline at 1-800-829-1040.

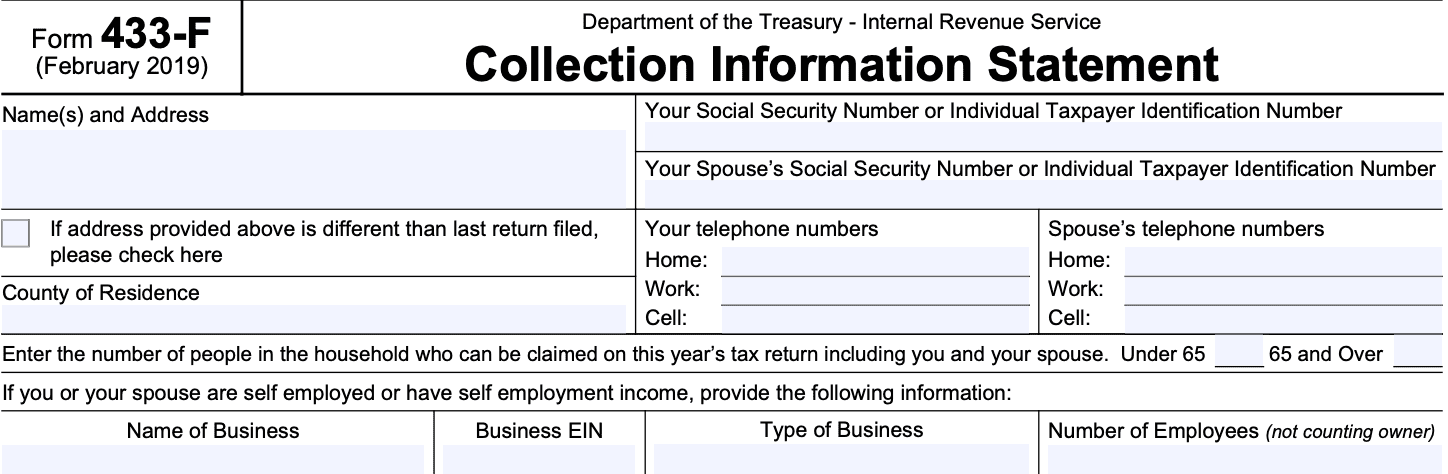

Step 2: Provide personal information.

At the top of the form, enter your personal information, including your name, Social Security number (SSN), address, and contact information. If you are married and filing jointly, include your spouse's information as well.

Step 3: Fill out the financial sections.

The majority of the form is dedicated to gathering your financial information. Here are the key sections to complete:

a. Section 1: Income

Provide details about your income sources, such as employment wages, (link: https://fincent.com/blog/1099-tax-calculator-for-self-employed-workers-and-independent-contractors text: self-employment income), rental income, retirement benefits, and any other sources of income you receive.

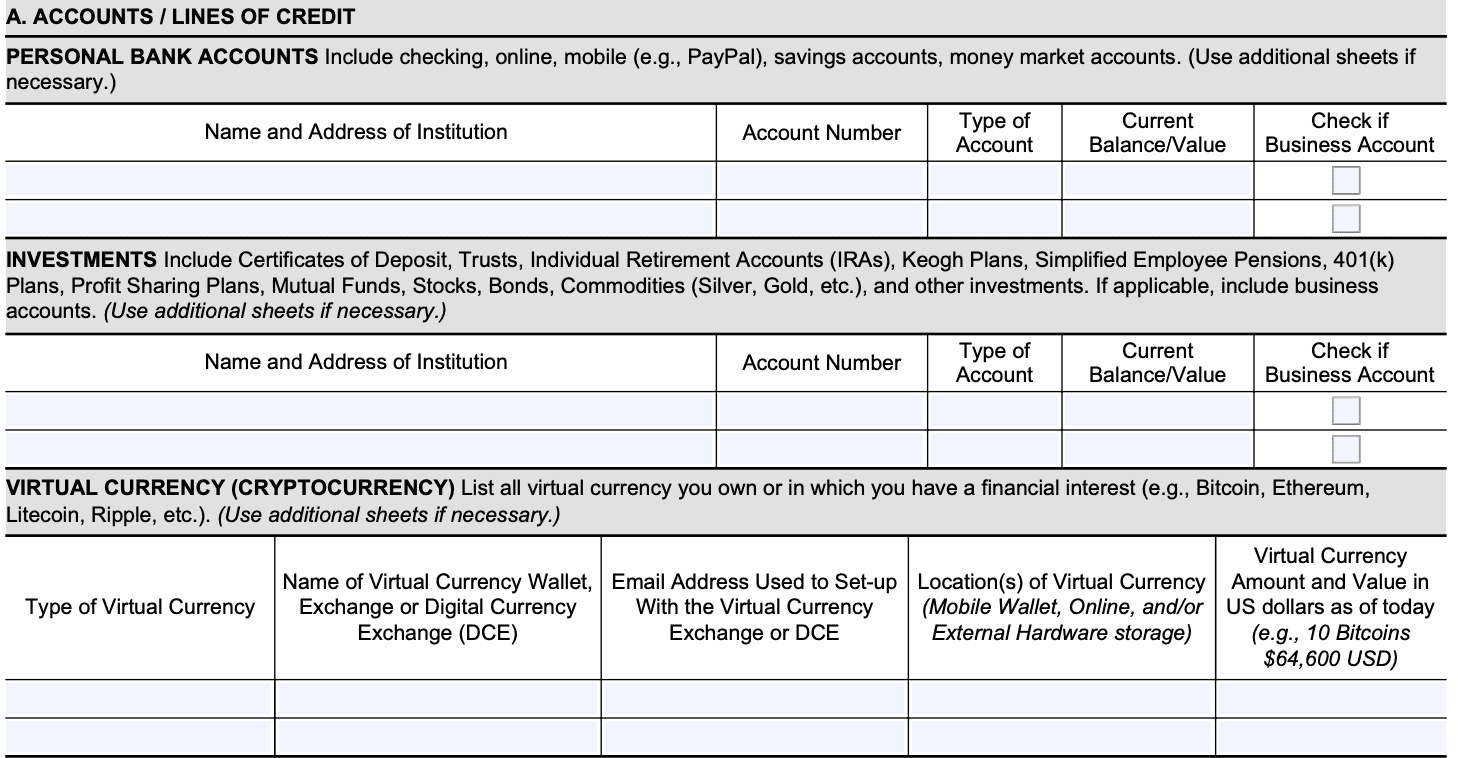

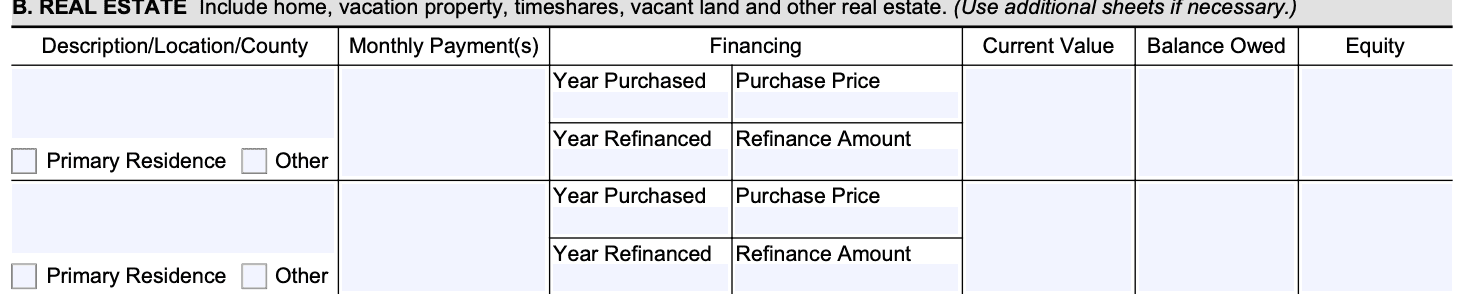

b. Section 2: Assets

List your assets, including bank accounts, investments, real estate, vehicles, and other valuable items you own. Be thorough and provide accurate information.

c. Section 3: Expenses

Document your monthly expenses, including housing costs (rent or mortgage payments), utilities, transportation, food, medical expenses, insurance, and other necessary living expenses.

d. Section 4: Other financial information

This section requires you to disclose information about any outstanding loans, credit card debts, and other financial obligations you have.

Step 4: Provide supporting documentation.

To support the financial information you provided, attach relevant documents, such as pay stubs, bank statements, tax returns, loan statements, and any other documentation that verifies your income, expenses, and assets.

Step 5: Review and sign the form.

Carefully review all the information you have provided on the form. Ensure that everything is accurate and up-to-date. Sign and date the form where indicated.

Step 6: Submit the form.

Make a copy of the completed form and all supporting documents for your records. Mail the original form and attachments to the IRS address provided in the form's instructions. Consider sending it via certified mail to have proof of delivery.

It's worth noting that completing Form 433-F can be complex, and if you're unsure about any aspect of the form or need personalized guidance, it's advisable to consult with a tax professional or an attorney specializing in tax matters.

Schedules/Deductions for Form 433-F

Here are some important schedules & deductions that may be included in Form 433-F:

Schedules for form 433-F

Depending on the taxpayer's financial situation, the following schedules may be included with Form 433-F:

- (link: https://fincent.com/irs-tax-forms/schedule-a-itemized-deductions text: Schedule A): Real Estate

- Schedule B: Personal Property

- (link: https://fincent.com/irs-tax-forms/schedule-c-profit-or-loss-from-business text: Schedule C): Wage and Salary

- (link: https://fincent.com/irs-tax-forms/schedule-d text: Schedule D): Self-Employment Income

- Schedule E: Other Income

- Schedule F: Expenses

- Schedule G: Installment Agreement

- Schedule H: Financial Accounts

- Schedule I: Trust Fund Recovery Penalty

- Schedule J: Joint Debtor

Deductions on form 433-F

Deductions can be claimed on Schedule F: Expenses. Some common deductions include:

- Housing and utilities expenses

- Vehicle operation expenses

- Health insurance premiums

- Childcare expenses

- Court-ordered payments (e.g., alimony, child support)

- Other necessary living expenses

It's important to note that the specific requirements, schedules, and deductions on Form 433-F may vary depending on the taxpayer's circumstances and the type of tax debt involved.

Common Mistakes To Avoid While Filing Form 433-F

When filing Form 433-F, which is the Collection Information Statement, it's important to be thorough and accurate to ensure your financial information is correctly reported. Here are some common mistakes to avoid while filing Form 433-F:

Incomplete or missing information: Make sure to fill out all the required fields on the form. Leaving out important details or providing incomplete information can lead to delays or rejections.

**Incorrect calculations: **Double-check all your calculations to ensure accuracy. Errors in income, expenses, or asset valuations can raise red flags and may result in additional scrutiny or incorrect determination of your ability to pay.

Inconsistent information: Be consistent with the information you provide on Form 433-F. Cross-check your income, expenses, and asset values to ensure they align with supporting documentation like pay stubs, bank statements, and tax returns.

Neglecting to attach supporting documentation: Form 433-F requires supporting documentation to substantiate the information provided. Failing to include necessary documents like tax returns, bank statements, and proof of expenses can delay the processing of your form.

Failure to update the form: If there are changes to your financial situation while your Form 433-F is being processed, it's important to notify the IRS promptly. Neglecting to update your form with accurate information can lead to complications and potential penalties.

Not reviewing the form before submission: Carefully review your completed Form 433-F before submitting it to the IRS. Look for any errors, omissions, or inconsistencies. Taking the time to review the form can help prevent unnecessary issues.

Missing the deadline: Ensure you submit your Form 433-F by the designated deadline. Failing to meet the deadline can result in additional penalties or missed opportunities for resolving your tax liabilities.

Remember, Form 433-F is a critical document that helps the IRS assess your financial situation. It's important to be honest, accurate, and thorough to avoid complications and ensure the best possible outcome.

How To File Form 433-F: Offline/Online/E-Filing

Here's an overview of the different ways you can file Form 433-F:

Offline

To file Form 433-F offline, you will need to print a copy of the form, fill it out manually, and mail it to the IRS. Here are the steps:

a. Obtain a copy of Form 433-F: You can download the form from the official IRS website or request a copy by calling the IRS at their toll-free number: 1-800-829-3676.

b. Fill out the form: Provide accurate and complete information on your income, expenses, assets, liabilities, and other financial details as requested on the form. Follow the instructions provided with the form to ensure you complete it correctly.

c. Gather supporting documentation: You may need to include supporting documentation such as pay stubs, bank statements, mortgage statements, and other financial records to substantiate the information provided on the form. Make copies of these documents to send along with your completed Form 433-F.

d. Mail the form: Once you have filled out the form and gathered the necessary documentation, mail the completed package to the appropriate IRS address. The specific address to which you should mail your form will depend on your location and the type of tax debt you have. You can find the correct mailing address in the instructions accompanying the form or on the IRS website.

Online/E-filing

The IRS does not currently offer the option to electronically file Form 433-F directly through their website. However, the IRS provides an online tool called the Online Payment Agreement (OPA) application, which allows you to apply for an installment agreement and provide some financial information.

It may streamline the process and reduce the need for Form 433-F in certain cases. To access the OPA application, visit the IRS website and search for "Online Payment Agreement."

It's important to note that IRS procedures and options can change over time, so it's always a good idea to visit the official IRS website or consult with a tax professional for the most up-to-date information and guidance regarding filing Form 433-F.

Conclusion

Form 433-F, the Collection Information Statement, is an essential document used by the IRS to assess a taxpayer's ability to pay their outstanding tax liabilities. By providing a comprehensive overview of your financial situation, this form helps the IRS determine the most appropriate course of action for collecting the debt.

When completing Form 433-F, it is crucial to be accurate and thorough in documenting your income, expenses, assets, and liabilities. Keep in mind that the information you provide may influence the IRS's decision on repayment options or other collection actions.

If you find the process overwhelming or need assistance, consider consulting a tax professional or seeking guidance from the IRS itself. Remember, addressing tax debts in a timely and responsible manner can help alleviate financial stress and ensure a smoother resolution process.